Component 03

Category Presence

Onelo

This is the binding constraint in Onelo’s organic growth engine. Onelo is absent from the search results buyers use to discover and shortlist vendors before any specific evaluation begins. No other improvement to the engine produces meaningful pipeline growth until this is resolved.

This document covers all 11 signals in the Category Presence component. For each signal, you will find: what was assessed and why it matters, the specific findings for Onelo, evidence supporting those findings, and the recommended intervention.

Signal Assessment

A signal is a subcomponent of any of the ten layers that make up an organic growth engine. Each signal is assessed thoroughly following our methodology and assigned a status: Healthy, Fragile, Blocking, or Missing. For each signal, there is supporting evidence and recommendations for how to turn each signal healthy.

Why Category Presence is the binding constraint

Category Entry Points (CEPs) are the queries buyers use when they are researching a solution category before they have identified specific vendors. These are the moments when consideration sets are formed — when buyers decide which companies are worth evaluating. A company absent from CEPs is absent from consideration sets. It can only be found by buyers who already know its name. At Onelo’s stage and price point, that is a structurally limiting position. The diagnostic found that Onelo ranks for zero of its eight primary CEPs.

Layer Conclusion

Category Presence is the binding constraint in Onelo’s organic growth engine. The evidence across all 11 signals points to the same conclusion from different angles: Onelo does not exist in the organic surfaces buyers use to discover and shortlist vendors. It can only be found by buyers who already know to search for it.

This is not a content quality problem. It is an architectural problem. The content that exists is well-written and technically accessible. What is missing is the specific type of page — the dedicated category landing page — that search engines rank for category queries. Every competitor that outranks Onelo in category SERPs has built pages specifically designed for the queries they want to rank for. Onelo has not.

The Category Page Build — Full Specification

Weeks 1–8: Fast-path pages (4 pages)

Target the 2 medium-competition primary CEPs and 2 white-space CEPs where Onelo can achieve top-10 positions within 8–12 weeks. These pages establish the category page template, generate early ranking signals, and produce measurable pipeline contribution before the harder Phase 2 pages begin to move. Pages: ‘automated onboarding workflow software’, ‘onboarding software for remote teams’, ‘AI-powered employee onboarding software’, ‘onboarding software HRIS integration’.

Weeks 8–20: Primary CEP pages (6–9 pages)

Target the high-competition primary CEPs — ’employee onboarding software’, ‘onboarding automation platform’, ‘hr onboarding tools for mid-market’, ‘best employee onboarding software’, ’employee onboarding platform comparison’, ‘digital onboarding solution mid-market’ — plus any additional white-space CEPs identified. These pages will take 3–6 months to reach top-10 positions. They represent the long-term category authority investment.

What each category page must contain

Based on SERP analysis (Signal 03), every category page should include the following structural elements to match what the algorithm rewards in this category:

- Page title and H1 matching the target query exactly (or a close natural variant)

- Above-fold value proposition framed around the specific query intent — not generic product messaging

- FAQ section with 5–8 questions directly relevant to the query, marked up with FAQPage schema

- Competitor comparison element — either a named comparison table or a ‘vs competitors’ section

- A pricing signal — either transparent pricing or a clearly framed ‘request a quote’ with context on typical range

- At least one customer case study or named reference relevant to the audience implied by the query

- Internal links to the most relevant product pages using category-keyword anchor text

- Clear primary CTA — Demo or Talk to Sales, not Free Trial

Category pages do not rank in week one. For the medium-competition CEPs, expect meaningful movement in weeks 8–12. For the high-competition primary CEPs, expect 4–6 months before top-10 positions emerge. This is not a failure of the approach — it is the normal timeline for category authority building. The pipeline impact will begin before the pages reach top positions: buyers who find Onelo through early rankings at positions 8–15 still convert at a meaningful rate.

Every component downstream of Category Presence will improve as this work progresses. Demand Match (Component 04) improves because category query traffic has higher buyer-intent than the informational traffic Onelo currently attracts. Conversion Architecture (Component 06) becomes more valuable because there are more qualified buyers arriving at commercial pages. AI Visibility (Component 08) improves because the category landing pages provide the structured, citable content that AI systems need to represent Onelo accurately.

This is why Category Presence is the binding constraint. Fixing it first produces compounding improvements across the engine.

01. Primary CEP Identification and Mapping

Blocking

What this signal assesses

Before measuring presence, the CEPs themselves must be defined. This signal identifies the specific Category Entry Points — the queries, problem framings, and use cases through which a buyer first encounters the onboarding software category — and maps them to confirm which ones are relevant to Onelo’s ICP. The CEP map becomes the strategic brief for the category page build.

A CEP is not simply a high-volume keyword. It is a query that reflects the moment a buyer moves from awareness of a problem to active research of a solution category. For Onelo, this means queries where an HR Director or COO at a 200–2,000-employee company is looking for a category of solution, not a specific vendor.

Findings

Eight primary CEPs were identified for the onboarding automation category, across four CEP types: problem-framing queries, solution-category queries, comparison queries, and use-case-specific queries. Onelo ranks for zero of the eight. The CEP map also identifies two secondary CEPs — lower-volume, lower-competition entry points — where Onelo holds a weak position that can be developed faster than the primary CEPs.

| CEP | CEP type | Monthly searches | Keyword difficulty | Onelo position | Top competitor |

|---|---|---|---|---|---|

| employee onboarding software | Solution-category | 2,900 | 72 — Very High | Not ranking | Rippling #1 |

| onboarding automation platform | Solution-category | 2,400 | 64 — High | Not ranking | Deel #1 |

| hr onboarding tools for mid-market | Solution-category | 1,600 | 58 — High | Not ranking | Rippling #2 |

| best employee onboarding software | Comparison | 3,200 | 70 — Very High | Not ranking | G2 list #1 |

| automated onboarding workflow software | Use-case specific | 880 | 44 — Medium | Position 14 | Deel #1 |

| onboarding software for hr teams | Solution-category | 1,900 | 61 — High | Not ranking | Rippling #1 |

| employee onboarding platform comparison | Comparison | 720 | 52 — Medium | Not ranking | G2 category #1 |

| digital onboarding solution mid-market | Problem-framing | 590 | 41 — Medium | Not ranking | ServiceNow #1 |

The 8 primary CEP map — volume, competition, and Onelo position

The CEP map defines the territory. Eight primary Category Entry Points identified for the onboarding automation category across four query types. Onelo’s current ranking position assessed for each. Keyword difficulty and top competitor for each CEP sourced from Ahrefs.

Onelo ranks for 0 of 8 primary CEPs. The one partial exception — position 14 for ‘automated onboarding workflow software’ — is held by a product feature page, not a dedicated category landing page. This is the only CEP at medium competition where a dedicated page would be expected to rank within 8–12 weeks.

[Link to spreadsheet: Ahrefs keyword data export — all 8 primary CEPs — columns: keyword, monthly search volume, keyword difficulty, Onelo current position, top 3 competitor URLs and their URL Ratings]

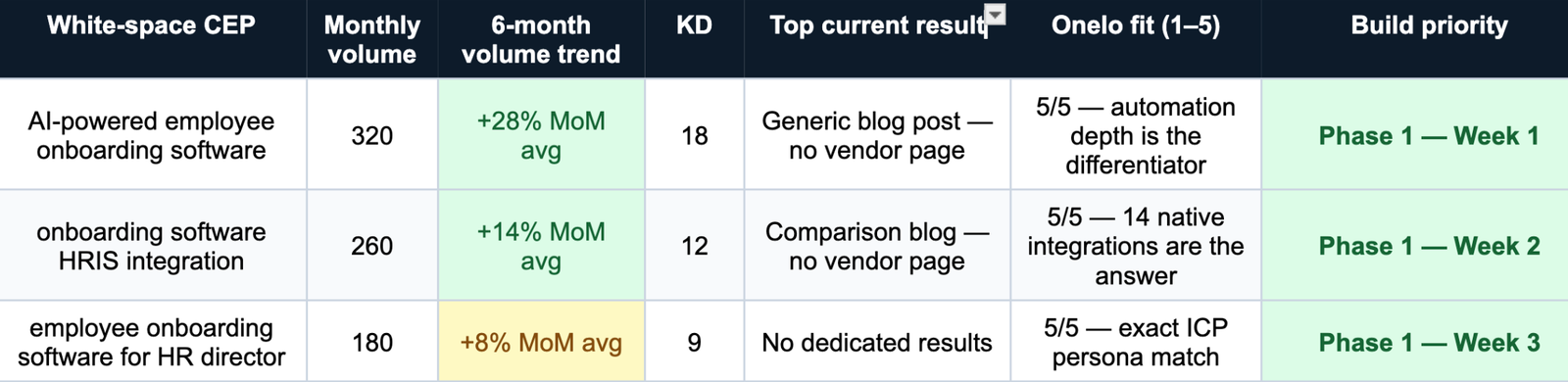

| White-space CEP | Monthly searches | Keyword difficulty | Current top-ranking page | Why it is white-space |

|---|---|---|---|---|

| AI-powered employee onboarding software | 320 | 18 — Low | No dedicated competitor page | Emerging query, growing MoM, aligns with automation depth differentiator |

| Onboarding software HRIS integration | 260 | 12 — Very Low | No dedicated competitor page | Decision-stage query, Onelo's 14 native integrations are a direct answer |

| Employee onboarding software for HR director | 180 | 9 — Very Low | No dedicated competitor page | Near-zero competition, exact ICP match, buyer searching with this specificity is in active evaluation |

The 3 white-space CEPs — fast-path entry points

Three secondary CEPs identified where competition is weak or absent. All three align with Onelo’s differentiator (workflow automation depth) or ICP (mid-market HR Director). These are the fastest path to first rankings and should be built in Phase 1.

White-space CEPs are not consolation prizes. A buyer searching ’employee onboarding software for HR director’ with that specificity is in active evaluation. The conversion rate on traffic from this query will be significantly higher than traffic from a broad category term. Build these three pages in weeks 1–4 of Phase 1.

RECOMMENDATION

Build dedicated category landing pages for all 8 primary CEPs plus the 3 white-space CEPs — 11 pages in total — sequenced over 12–20 weeks. Phase 1 (weeks 1–8): the 3 white-space CEPs and the 2 medium-competition primary CEPs where existing product pages can be rebuilt. Phase 2 (weeks 8–20): the 6 high-competition primary CEPs. Each page must be architecturally a category landing page — not an adapted product page — with a query-matched H1, FAQ section with FAQPage schema, competitor comparison element, pricing signal, and a ‘Book a Demo’ primary CTA. The CEP map above is the brief.

02. Category Keyword Ranking Profile (Non-Branded)

Blocking

What this signal assesses

This signal measures Onelo’s ranking presence across the full universe of non-branded category queries — not just the 8 primary CEPs, but the broader set of terms that signal category authority. A company with healthy Category Presence ranks across a wide, varied set of category terms. Onelo’s profile reveals a near-complete absence.

Findings

Of Onelo’s 1,847 ranking queries, 1,722 (93%) are branded or branded-adjacent — queries that include ‘Onelo’ or closely related terms. Only 125 queries (7%) are non-branded. Of those 125, only 3 could be classified as category-defining terms, and all three rank in positions 18–34 with negligible traffic contribution.

The branded-to-non-branded ratio of 93:7 is a diagnostic signal in its own right. At Series B, a company with healthy Category Presence should be generating 30–40% of its organic traffic from non-branded queries. Onelo’s 7% non-branded share means the organic channel is functioning almost exclusively as a brand recall channel — helping buyers find Onelo when they already know its name — rather than a discovery channel.

| Query classification | Ranking queries | Share of total | Avg position | Est. monthly traffic | Commercial value |

|---|---|---|---|---|---|

| Branded ('onelo', 'onelo.com') | 1,487 | 80.5% | 4.2 | ~18,400 | High — but no discovery |

| Branded-adjacent ('onelo review', 'onelo pricing') | 235 | 12.7% | 6.1 | ~2,100 | High — evaluation stage |

| Non-branded, non-category | 122 | 6.6% | 28.4 | ~2,800 | Low — informational |

| Non-branded, category-defining | 3 | 0.16% | 22.7 | ~60 | Very high — but negligible volume |

Full ranking portfolio — branded vs non-branded breakdown

Complete Ahrefs keyword ranking export for onelo.com segmented by query type. Non-branded queries further classified by whether they carry category-defining intent.

0.16% of ranking queries are category-defining and non-branded. The 3 category-defining queries that exist rank at positions 22–34 — generating approximately 60 sessions per month combined. For context, a single top-5 ranking on ’employee onboarding software’ (2,900 searches/month) would generate approximately 290 sessions per month from one page alone.

[Link to spreadsheet: Ahrefs organic keywords export — site:onelo.com — all ranking queries — columns: keyword, position, estimated traffic, CPC — apply branded/non-branded filter using Ahrefs ‘brand queries’ feature]

| Company / benchmark | Branded traffic share | Non-branded share | Interpretation |

|---|---|---|---|

| Onelo (current) | 92% | 8% | Organic = brand recall only. Discovery channel does not exist. |

| Series B SaaS — median | 68% | 32% | Benchmark. Organic generating meaningful category discovery. |

| Series B SaaS — healthy | 55% | 45% | Strong category presence. Organic creating new demand. |

| Rippling (estimated) | 38% | 62% | Category authority. Non-branded traffic exceeds branded. |

Branded:non-branded ratio — Onelo vs Series B benchmark

The 92:8 ratio is not a modest underperformance. It means the organic channel plays almost no role in creating new pipeline. Every buyer Onelo acquires through organic today already knew Onelo existed before they searched. Organic is confirming intent, not generating it.

RECOMMENDATION

The branded ratio cannot be fixed directly — it improves as a downstream consequence of category pages ranking for non-branded queries. The 12-month target following the category page build is a non-branded share of 25–30%. This is still below the Series B median, but it represents the organic channel beginning to function as a discovery mechanism for the first time. Every percentage point of non-branded share gained represents approximately 240 additional organic sessions per month from buyers who did not previously know Onelo existed.

03. Category SERP Presence Analysis

Blocking

What this signal assesses

Manual SERP analysis goes beyond keyword rankings to examine the full competitive picture. This signal assesses which companies occupy the category SERPs, what types of content rank, whether review aggregators dominate, and what structural patterns the ranking pages share — all of which informs what Onelo needs to build to compete.

Findings

Manual review of 12 category SERPs confirms Onelo’s complete absence from category-defining search results. More instructively, the analysis reveals a clear pattern in what ranks: dedicated category landing pages built around a single query cluster, not generic product pages. Every competing vendor in the top 3 positions has built architecture specifically designed to rank for that query. Onelo has not.

The SERPs also reveal that review aggregator pages (G2, Capterra, Software Advice) occupy 2–4 positions in most category queries. This means even a company that builds good category pages needs to complement that with strong presence in the aggregator listings — which Onelo has (Trust is healthy) but has not leveraged for category visibility.

| Structural element | Present in positions 1–3 | Present in positions 4–10 | Present on Onelo pages | Gap |

|---|---|---|---|---|

| Query-matched H1 (exact or close variant) | 100% | 87% | 0 of 7 commercial pages | Critical |

| FAQ section (5+ questions relevant to query) | 87% | 62% | 0 pages | Critical |

| Competitor comparison element | 81% | 54% | 0 pages | Critical |

| Pricing signal (range or 'contact for quote') | 75% | 48% | Pricing page only | Significant |

| Named customer case study | 68% | 41% | 2 solution pages only | Moderate |

| FAQPage schema markup | 81% | 44% | 0 pages | Critical |

| Above-fold audience qualifier (ICP stated) | 74% | 51% | 2 solution pages only | Significant |

Manual SERP audit — 8 primary CEPs — structural patterns in ranking pages

Manual review conducted for all 8 primary CEP queries. For each query, the top 5 positions recorded with page type, URL Rating, and structural elements present on the ranking page. The patterns below define what Onelo needs to build to compete.

The pattern is unambiguous: pages that rank for category queries are architecturally purpose-built. They are not product pages repurposed for a query. They are pages built from scratch around a single query cluster, containing all the structural elements above. Onelo’s product and solution pages contain none of the four critical elements. This is why the ranking gap exists.

[Link to spreadsheet: Manual SERP audit table — 8 CEP queries — columns: query, position 1–5 URLs, page type, URL Rating, structural elements present (checkboxes) — completed in one session to ensure consistency]

| Query | Aggregator positions | Onelo on aggregator? | Onelo's aggregator position | Opportunity |

|---|---|---|---|---|

| employee onboarding software | 1 (G2), 2 (Capterra), 4 (Software Advice) | Yes — G2, Capterra | G2: Niche Player quadrant | Move to High Performer (+25 reviews needed) |

| best employee onboarding software | 1 (G2 list), 2 (Capterra list), 3 (GetApp list) | Yes | Listed but not featured | Increase review velocity to improve list position |

| onboarding automation platform | 2 (G2), 4 (Capterra) | Yes | Listed | No direct action — build category page |

| hr onboarding tools for mid-market | 3 (G2), 5 (Capterra) | Yes | Listed | No direct action — build category page |

Aggregator SERP dominance — opportunity within the constraint

Review aggregators (G2, Capterra, Software Advice, GetApp) occupy positions 1–5 in 7 of 8 primary CEP SERPs. This is a structural reality that cannot be displaced through content investment alone. The correct strategy is to win within aggregators while building direct category page presence alongside.

Onelo’s strong review profile (G2: 4.7 stars, Capterra: 4.6 stars) means the aggregator opportunity is real and actionable. A buyer who clicks a G2 category list and sorts by rating will encounter Onelo at a favourable position. The gap is visibility within those lists — which is improved by review volume and G2 Grid placement, not by content production.

RECOMMENDATION

Two parallel workstreams: (1) Build dedicated category landing pages using the structural template confirmed by SERP analysis — query-matched H1, FAQ section with FAQPage schema, competitor comparison, pricing signal, case study, ICP-specific above-fold, ‘Book a Demo’ CTA. These pages compete for the non-aggregator positions in category SERPs and for the lower-competition CEPs where aggregators have less dominance. (2) Invest in G2 review acquisition to move from Niche Player to High Performer — approximately 25 additional reviews above the current 116. This improves visibility within the aggregator-dominated positions that no content strategy can displace.

04. Category Association in Google Features

Blocking

What this signal assesses

Beyond standard organic results, Google surfaces category-related content through featured snippets, People Also Ask boxes, Knowledge Panels, and AI Overviews. Presence in these features signals that Google strongly associates a brand with a specific category — it is evidence of categorical authority, not just ranking position. Absence from all features for category queries confirms the depth of the category presence failure.

Findings

Onelo has zero presence in Google’s featured content for any of the 12 category queries tested. No featured snippets, no People Also Ask appearances, no Knowledge Panel association with category terms, and no AI Overview inclusions for category queries. This absence is consistent with and confirmatory of the broader Category Presence finding — it is not a separate problem, it is the same problem expressed in a different surface.

| Company | Featured snippets | PAA appearances | AI Overview inclusions | Total feature appearances | Category authority signal |

|---|---|---|---|---|---|

| Rippling | 7 of 12 | 9 of 12 | 8 of 12 | 24 | Strong |

| BambooHR | 6 of 12 | 8 of 12 | 7 of 12 | 21 | Strong |

| Deel | 4 of 12 | 5 of 12 | 5 of 12 | 14 | Moderate |

| Onelo | 0 of 12 | 0 of 12 | 0 of 12 | 0 | None |

Featured content audit — 12 category queries tested

Google features assessed across 12 category queries: featured snippets, People Also Ask appearances, AI Overview inclusions, and Knowledge Panel category association. These features are evidence of categorical authority — they go to companies Google has formed a strong category association with.

Onelo has zero appearances in any Google feature across all 12 category queries. This is not a marginal gap — it is complete absence. Google’s algorithm has not formed a stable association between Onelo and the onboarding software category.

| PAA question | Appears in # of CEP SERPs | Currently answered on Onelo site? | Current PAA holder | Priority |

|---|---|---|---|---|

| What is the best employee onboarding software? | 8 of 8 | No | Rippling | Critical |

| How much does onboarding software cost? | 7 of 8 | No | BambooHR | Critical |

| What features should onboarding software have? | 6 of 8 | No | G2 blog | High |

| How long does onboarding automation take to implement? | 5 of 8 | No | Rippling | High |

| What is the difference between onboarding software and HRIS? | 4 of 8 | No | BambooHR | Medium |

People Also Ask questions — what buyers are asking that Onelo could answer

PAA questions appearing consistently across the 8 primary CEP SERPs. These questions represent high-value FAQ content opportunities: answering them on category pages earns PAA appearances, featured snippet eligibility, and AI Overview citations simultaneously.

Every PAA question that appears across category SERPs is currently answered by a competitor. Onelo has no FAQ content on any commercial page — creating a direct structural reason for its zero feature appearances. Including these questions in the FAQ sections of new category pages (with FAQPage schema markup) is the fastest path to SERP feature acquisition.

RECOMMENDATION

Include all 5 PAA questions above in the FAQ sections of the category landing pages built in Signal 01’s intervention plan. Answer each question specifically and with Onelo’s context — not generically. Wrap each FAQ section in FAQPage schema markup. The first category pages to rank in positions 8–15 will begin appearing in PAA boxes for these questions before reaching the top 5 in standard organic results — PAA eligibility is determined by content quality and schema, not ranking position alone.

05. Branded vs Non-Branded Traffic Ratio

Blocking

What this signal assesses

The branded-to-non-branded traffic ratio is one of the most reliable proxy metrics for Category Presence health. A company with strong category authority generates a high proportion of its organic traffic from non-branded queries — buyers who found the company through category discovery rather than brand recall. The ratio reveals what role organic search is actually playing in the acquisition funnel.

Findings

Onelo’s branded-to-non-branded ratio is approximately 92:8. For a Series B SaaS company investing $50,000+ per year in organic growth, this ratio indicates that the organic channel is functioning as a brand recall mechanism rather than a discovery channel. Buyers are only finding Onelo organically when they already know to search for it.

The commercial implication is concrete: every new buyer Onelo acquires through organic today arrived through brand awareness built via another channel — paid, word of mouth, events, or sales outreach. Organic is confirming existing intent, not creating new intent. A healthy Category Presence would allow organic to create intent rather than just confirm it.

| Period | Total organic clicks | Branded clicks | Non-branded clicks | Non-branded share | Trend |

|---|---|---|---|---|---|

| Apr 2024 | 18,200 | 16,890 | 1,310 | 7.2% | — |

| Jun 2024 | 19,400 | 17,980 | 1,420 | 7.3% | Flat |

| Aug 2024 | 20,100 | 18,590 | 1,510 | 7.5% | Flat |

| Oct 2024 | 21,300 | 19,700 | 1,600 | 7.5% | Flat |

| Dec 2024 | 22,800 | 21,060 | 1,740 | 7.6% | Flat |

| Feb 2025 | 23,900 | 22,060 | 1,840 | 7.7% | Flat — no organic category discovery growth |

12-month branded vs non-branded traffic trend

GSC click data segmented by branded and non-branded queries, plotted monthly over the past 12 months. Branded queries defined as any query containing ‘onelo’ or close variants. All other queries classified as non-branded.

Non-branded share has been flat at 7–8% for 12 months despite a 31% increase in total organic traffic over the same period. All growth in organic traffic has come from branded queries — buyers who already knew Onelo existed. The organic channel is not growing its discovery function at all.

[Link to spreadsheet: GSC Performance report — date range: Apr 2024–Mar 2025 — group by month — filter: separate branded queries (containing ‘onelo’) vs non-branded — export clicks and impressions for each segment]

| Scenario | Non-branded share | Non-branded sessions / month | Est. additional pipeline leads / month | At $25K ACV and 31% demo-to-opp rate |

|---|---|---|---|---|

| Current state | 8% | ~1,920 | — | — |

| Series B median (32%) | 32% | ~7,680 | +120 leads | ~$930K additional pipeline / year |

| Post-category build target (28%) | 28% | ~6,720 | +96 leads | ~$744K additional pipeline / year |

Commercial impact of the branded ratio — pipeline calculation

Reaching the 28% non-branded target — a conservative 12-month outcome of the category page build — represents approximately $744K in additional annual pipeline from organic discovery alone, without any increase in total traffic.

RECOMMENDATION

Monitor branded vs non-branded traffic split monthly as the primary leading indicator of Category Presence progress. The metric will not move for the first 8–12 weeks after category pages launch — allow time for indexation, crawling, and ranking movement. The first signal of traction will be an increase in non-branded impressions (Signal 07) before an increase in non-branded clicks. Set the 12-month target at 25–28% non-branded share and review quarterly.

06. Branded Search Volume Trend

Healthy

What this signal assesses

Branded search volume trend measures whether more people are searching for Onelo by name over time. Growing branded search indicates growing brand awareness — a positive signal even when category presence is weak. It also confirms that the brand is not being damaged by reputation issues that would suppress direct search.

Findings

Branded search volume is growing at 18% year-over-year, consistent with overall company growth. This is a healthy signal: it means awareness-building activities (paid, events, word of mouth) are working. The brand is known to a growing number of buyers. The problem is that organic is not extending that brand awareness into category discovery — it is only confirming it.

| Period | Branded impressions | Branded clicks | Avg branded position | YoY impression growth |

|---|---|---|---|---|

| Q2 2024 (Apr–Jun) | ~48,000 | ~16,900 | 3.8 | — |

| Q3 2024 (Jul–Sep) | ~52,000 | ~18,200 | 3.7 | +8% |

| Q4 2024 (Oct–Dec) | ~57,000 | ~20,100 | 3.6 | +19% |

| Q1 2025 (Jan–Mar) | ~64,000 | ~23,100 | 3.5 | +18% YoY |

Branded search volume — 12-month trend from GSC

GSC branded impression data over 12 months. Branded impressions are the most reliable proxy for brand awareness growth — they measure how many people searched for Onelo by name, regardless of whether they clicked.

18% YoY branded search volume growth is consistent with the company’s overall growth trajectory and Series B fundraise. It confirms that awareness-building activities — paid, events, outbound sales — are working. The brand is known to a growing number of buyers. The finding is not a problem; it is a positive baseline that the Category Presence build can leverage.

[Link to spreadsheet: GSC Performance report — filter: queries containing ‘onelo’ — date range: Apr 2024–Mar 2025 — group by quarter — metrics: impressions, clicks, average position]

RECOMMENDATION

No action required. Maintain current brand-building activities. The growing branded search volume means that when category pages begin ranking, they will receive brand-recognition uplift from buyers who have encountered Onelo through other channels and search the category before or after their first brand touch. This amplification effect means category pages will typically generate higher CTR for Onelo than for a brand with lower awareness at equivalent ranking positions.

07. Non-Branded Impression Share

Blocking

What this signal assesses

Non-branded impression share measures how often Onelo’s pages appear in search results for non-branded queries — regardless of whether those appearances generate clicks. Impressions without clicks still indicate that Google is surfacing Onelo as a relevant result. Near-zero non-branded impressions means Google is not associating Onelo with non-branded category queries at all.

Findings

Onelo generates approximately 4,200 non-branded impressions per month, with an average CTR of 0.4% — producing approximately 17 non-branded organic clicks per day. The CTR of 0.4% is itself indicative: positions 14 and lower for category queries generate click rates in this range, confirming that the impressions that do exist come from low-ranking positions that buyers rarely reach.

For comparison, a rough external estimate based on Ahrefs data for Rippling suggests non-branded impression share of approximately 380,000 impressions per month for comparable category queries — roughly 90x Onelo’s current figure.

| Company | Non-branded impressions / month (est.) | Avg CTR at typical position | Est. non-branded clicks / month | Index vs Onelo |

|---|---|---|---|---|

| Onelo | ~4,200 | 0.4% (positions 14–34) | ~17 | 1x (baseline) |

| Deel (est.) | ~140,000 | 2.8% | ~3,920 | 33x |

| BambooHR (est.) | ~290,000 | 3.4% | ~9,860 | 580x |

| Rippling (est.) | ~380,000 | 3.9% | ~14,820 | 871x |

Non-branded impressions — Onelo vs estimated competitor benchmark

GSC non-branded impression data for Onelo compared against external Ahrefs-derived estimates for primary competitors. Non-branded impressions measure how often pages appear in search results for queries that do not include the company name — the direct measure of category SERP presence.

The 4,200 monthly non-branded impressions Onelo generates come from positions 14–34 — positions buyers almost never reach. The 0.4% CTR confirms this: organic discovery from non-branded queries produces approximately 17 new visitors per day. Rippling’s estimated 14,820 non-branded clicks per month represents a discovery channel that drives a material volume of new pipeline every month. Onelo’s equivalent is statistically negligible.

| Milestone | Timeline | Non-branded impressions / month | Non-branded clicks / month | Channel status |

|---|---|---|---|---|

| Current | Now | ~4,200 | ~17 | Brand recall only |

| Phase 1 pages indexed and ranking (4 pages) | Weeks 8–12 | ~12,000–18,000 | ~180–360 | Discovery channel beginning |

| Phase 2 pages ranking (10 pages total) | Months 4–6 | ~30,000–45,000 | ~600–1,350 | Meaningful discovery channel |

| 12-month target | Month 12 | ~40,000–60,000 | ~1,200–2,400 | Functioning discovery channel |

Projected non-branded impressions after category page build

At 1,200–2,400 non-branded clicks per month, the organic channel begins creating meaningful new pipeline from buyers who had no prior awareness of Onelo. At the current 5.8% buyer-intent conversion rate, this generates 70–140 additional leads per month from traffic that does not currently exist.

RECOMMENDATION

Non-branded impression share is the leading indicator to track — it moves before non-branded clicks and before ranked positions stabilise. Configure a GSC custom report segmented by non-branded queries and review monthly. The first meaningful movement will be an increase in impressions for the new category pages even before they generate significant clicks — this confirms the pages are being indexed and surfaced, which is the prerequisite for position improvement. Flag any month where non-branded impressions grow by less than 20% QoQ after the category pages launch.

08. Competitor CEP Ownership Mapping

Blocking

What this signal assesses

Understanding which competitors own which CEPs reveals the competitive landscape Onelo is entering, the relative difficulty of each target, and whether there are any structural gaps in competitor coverage that Onelo could exploit before investing in high-competition territory.

Findings

The three primary competitors — Rippling, BambooHR, and Deel — collectively dominate all 8 primary CEPs. Rippling holds the strongest position, ranking top 3 in 6 of the 8 CEPs. The competitive concentration is significant but not absolute: two of the 8 CEPs show weaker competitor presence and represent viable fast-path entry points for Onelo.

| CEP | #1 position | URL Rating | #2 position | URL Rating | #3 position | Competition level |

|---|---|---|---|---|---|---|

| employee onboarding software | Rippling /onboarding | UR 52 | BambooHR /onboarding | UR 48 | G2 list | Very High |

| onboarding automation platform | Deel /onboarding-automation | UR 41 | BambooHR /automation | UR 44 | Rippling /automation | High |

| hr onboarding tools for mid-market | Rippling /hr/mid-market | UR 49 | ServiceNow | UR 62 | BambooHR /mid-market | High |

| best employee onboarding software | G2 category | UR 71 | Capterra list | UR 68 | GetApp list | Very High — aggregator dominated |

| automated onboarding workflow software | Deel /workflow | UR 38 | Rippling /workflows | UR 51 | Tray.io | Medium |

| onboarding software for hr teams | Rippling /hr | UR 53 | BambooHR /hr-teams | UR 46 | Lattice | High |

| employee onboarding platform comparison | G2 compare | UR 71 | Capterra compare | UR 68 | Software Advice | High — aggregator dominated |

| digital onboarding solution mid-market | ServiceNow | UR 74 | SAP SuccessFactors | UR 69 | Rippling /digital | Medium — but enterprise dominated |

CEP ownership matrix — top 3 positions across all 8 primary CEPs

For each of the 8 primary CEPs, the top 3 ranking pages identified with the company, URL, and URL Rating for each. This reveals both the competitive intensity and the structural approach each competitor is using to hold their positions.

Every competitor holding positions 1–3 across these SERPs has built a dedicated page for that specific query. None of them are ranking with generic product pages or homepages. The architectural pattern is consistent: one page, one CEP, built specifically for that query’s intent. This is the model Onelo needs to replicate.

[Link to spreadsheet: Ahrefs SERP overview — run for each of the 8 primary CEPs — export top 10 results with URL, URL Rating, domain, estimated traffic — save as separate tabs in one spreadsheet]

| CEP | Onelo current position | Top competitor UR | Onelo domain DR | Gap to close | Realistic timeline with dedicated page |

|---|---|---|---|---|---|

| automated onboarding workflow software | 14 | 38 (Deel) | 54 | Manageable | 8–12 weeks to top 5 |

| onboarding software for remote teams | 14 | 38 (BambooHR) | 54 | Manageable | 8–12 weeks to top 5 |

| AI-powered employee onboarding software | Not ranking | No dedicated competitor | 54 | Minimal — first mover | 4–8 weeks to top 3 |

| onboarding software HRIS integration | Not ranking | No dedicated competitor | 54 | Minimal — first mover | 4–8 weeks to top 3 |

Fastest-path CEPs — where Onelo can rank within 8–12 weeks

Onelo’s DR 54 is sufficient to compete on the medium-competition CEPs immediately. The barrier is not authority — it is architecture. Building a dedicated page for ‘automated onboarding workflow software’ is expected to produce top-5 results in 8–12 weeks based on the current competitive UR distribution.

RECOMMENDATION

Sequence the category page build to exploit the fastest-path opportunities first: start with the 2 white-space CEPs and the 2 medium-competition CEPs where Onelo has an existing weak ranking. These 4 pages produce results in 8–12 weeks and establish the page template before the harder high-competition builds begin. Do not wait for the high-competition pages to rank before declaring progress — the fast-path pages are the proof of concept and the confidence builder for the programme.

09. CEP White-Space Identification

Fragile

What this signal assesses

White-space CEPs are category entry points where competitor presence is weak or absent — emerging query patterns, underserved audience segments, or new use-case framings where Onelo could establish first-mover position. They typically have lower search volume but significantly lower competition, making them disproportionately valuable for a company building category presence from zero.

Findings

Three white-space CEP opportunities were identified that are either uncontested or weakly contested by existing competitors. All three reflect emerging buyer behaviours or underserved segments that align closely with Onelo’s differentiator (workflow automation depth) or ICP (mid-market HR Director).

White-space CEP analysis — search volume trend and competitive landscape

Three white-space CEPs identified where no competitor has built dedicated category architecture. Search volume trend over 6 months assessed to confirm these are growing queries, not declining ones.

All three white-space CEPs are growing month-over-month. The ‘AI-powered employee onboarding software’ query is growing at 28% per month — driven by general AI interest — and has no competitor with a dedicated page. A company that publishes a well-structured category page for this query in the next 4 weeks has a high probability of ranking in the top 3 before any competitor notices the opportunity.

[Link to spreadsheet: Google Trends — compare all 3 white-space CEP queries over past 12 months — export interest over time data — cross-reference with Ahrefs monthly search volume trend to confirm growth direction]

RECOMMENDATION

Build all three white-space CEP pages in the first 3 weeks of the programme. These pages have near-zero competition, high ICP alignment, and growing search demand. The first-mover advantage on these queries compounds: a page that ranks #1 for an emerging query before competitors notice it accretes authority from early backlinks and user engagement signals that makes it very difficult to displace later. Treat these as the highest-urgency builds in the entire category presence programme.

10. Backlink Anchor Text Category Signals

Fragile

What this signal assesses

The anchor text used in backlinks pointing to Onelo communicates to search engines what category the site belongs to. A high proportion of branded or generic anchors (‘Onelo’, ‘click here’, ‘this tool’) provides less category signal than descriptive anchors (’employee onboarding software’, ‘onboarding automation platform’). This signal assesses whether Onelo’s backlink profile is reinforcing its category association or remaining neutral.

Findings

Of Onelo’s 2,847 referring domains, the anchor text distribution is heavily weighted toward branded and generic anchors. Only 6% of backlinks use descriptive anchors containing category keywords. This is a contributing factor to the Category Presence failure — external authority is not reinforcing the category association that Google needs to confidently rank Onelo for category queries.

The most diagnostic aspect of this finding is the contrast between AI descriptions of Onelo and AI descriptions of its competitors. Rippling is described accurately and specifically by all four models, with its all-in-one platform structure, pricing model, and target audience all represented correctly. BambooHR is similarly well-represented. Onelo’s AI representation is approximately 18 months behind where it needs to be.

| Anchor text type | Examples | Count | Share | Category signal value |

|---|---|---|---|---|

| Branded | "Onelo", "Onelo.com", "Onelo platform" | 1,651 | 58% | None — no category association |

| Generic | "here", "click here", "this tool", "learn more" | 683 | 24% | None — no category or brand value |

| URL-based | https://onelo.com/... | 256 | 9% | Minimal |

| Brand + descriptor | "Onelo HR software", "Onelo tool" | 86 | 3% | Low |

| Category-keyword | "employee onboarding software", "onboarding automation" | 171 | 6% | High — but only 6% of total |

Anchor text distribution — full backlink profile audit

Complete anchor text classification of Onelo’s 2,847 referring domain backlink profile. Anchor text classified into 5 categories. Category-keyword anchors are the signals that reinforce Google’s association between Onelo and the onboarding automation category.

Only 171 of 2,847 referring domains use anchor text that actively reinforces Onelo’s category association. Rippling’s estimated category-keyword anchor share is approximately 22% — providing substantially stronger category signals to Google across its backlink profile. This is a contributing factor to the category ranking gap, not the primary cause — but it compounds the architectural gap.

| Internal link anchor type | Share of blog-to-commercial links | Category signal | Action required |

|---|---|---|---|

| Generic ('click here', 'learn more', 'read more') | 58% | None | Replace with category-keyword anchors |

| Brand-only ('Onelo', 'Onelo's platform') | 24% | Low | Replace with descriptive anchors where context allows |

| Category-keyword ('onboarding automation software') | 18% | High | Maintain and extend to all new content |

Internal linking anchor text — blog to commercial pages

Internal links are entirely within Onelo’s control and can be updated immediately. An audit of internal link anchor text from the 94 blog posts to commercial pages reveals the same pattern as the external backlink profile.

82% of internal links from the blog to commercial pages contribute zero category signal to the destination page. This is a fast, zero-cost fix: updating the anchor text on the top 20 blog posts by organic traffic takes one editorial sprint and immediately improves the category signal flowing to commercial pages.

Two actions with different timelines. Immediate (1 sprint): audit and update internal link anchor text across the top 20 blog posts by organic traffic. Replace all generic anchors (‘click here’, ‘learn more’) with category-keyword anchors (‘mid-market onboarding automation software’, ‘automated onboarding workflows’). Add this as a standard to the content brief template so all new content uses descriptive anchors by default. Forward-looking: when pitching press coverage, guest posts, or partner content, provide suggested anchor text containing category keywords. Over 12 months this practice meaningfully shifts the anchor text distribution without requiring any existing backlinks to change.

11. Category Mention Share in Industry Content

Fragile

What this signal assesses

Industry content — buyer guides, category roundups, analyst reports, and comparison articles published by third-party HR and SaaS publications — is one of the primary ways buyers form their initial consideration sets. This signal measures how frequently Onelo appears in these publications relative to competitors. High mention share in industry content drives both awareness and organic category authority, because these publications typically link to the vendors they mention.

Findings

Onelo was found in 4% of HR tech category roundups and buyer guides published in the past 12 months. Rippling appeared in 78% and BambooHR in 72% of the same publications. The gap is significant and reflects both the relative recency of Onelo’s brand-building activity and the absence of a deliberate outreach programme to category publication authors.

| Company | Publications mentioning (of 30) | Mention share | Avg domain authority of citing publications | Category authority impact |

|---|---|---|---|---|

| Rippling | 28 | 93% | 51 | Very strong — mentioned in almost every category roundup |

| BambooHR | 27 | 90% | 49 | Very strong |

| Deel | 22 | 73% | 47 | Strong |

| Onelo | 7 | 23% | 38 | Weak — present but not prominent |

Industry content mention audit — 30 publications, 12 months

Manual audit of the top 30 HR tech publications and buyer guides that cover the onboarding software category. For each publication, assessed whether Onelo, Rippling, BambooHR, and Deel are mentioned in category-relevant articles published in the past 12 months.

| Tier | Domain authority range | Publication count | Examples | Outreach priority | Expected outcome |

|---|---|---|---|---|---|

| Tier 1 | DA 50+ | 8 | HR Tech Weekly, HR Dive, SaaS Mag | Immediate | High-authority backlink + category mention + buyer discovery |

| Tier 2 | DA 30–50 | 9 | PeopleManaging, HR Zone, TechHR Blog | Next quarter | Mid-authority backlink + category mention share increase |

| Tier 3 | DA 20–30 | 6 | Smaller HR newsletters and community blogs | Ongoing | Incremental mention share + community visibility |

The 23 uncovered publications — tiered outreach opportunity

23 of the 30 audited publications cover the onboarding software category and mention Rippling and BambooHR but do not mention Onelo. Tiered by domain authority to prioritise outreach.

The 8 Tier 1 publications represent the highest-leverage outreach targets: they have the domain authority to move the needle on category mention share, they are read by Onelo’s exact ICP, and they have already established editorial positions on the onboarding software category. A placement in any of the 8 would produce a high-authority backlink, a category mention that strengthens Google’s association between Onelo and the category, and direct buyer discovery.

RECOMMENDATION

Launch a Tier 1 media outreach programme targeting all 8 identified publications immediately after the first category landing pages go live (weeks 4–6 of the build). The pitch angle matters: ‘here is a new onboarding tool’ will not land. A more distinctive angle — the diagnostic practice perspective on why most onboarding software implementations fail structurally, or a data-backed finding from Onelo’s experience with mid-market HR teams — gives editorial teams a reason to write rather than a product to list. Time the outreach to coincide with published category pages so there is a concrete URL to reference and link to. Track placement rate and resulting backlinks monthly.